The widespread use of OTTs by even the widespread man has remarkably reworked day-to-day dwelling and enhanced the standard of life generally. We couldn’t have pulled via the pandemic in addition to we did if it had not been for the OTT content material flowing via the telecom pipes. TRAI has issued a complete session paper dated July 7, 2023 on OTT companies and it’s fascinating to review the info supplied therein. OTTs successfully began showing in India in a major manner round 2014, and TRAI did its first session in 2015. Due to this fact, to look at the financial impacts of OTTs, it could be acceptable to check the telecom common income per person (ARPU) in 2022 to that in 2013. Such an in depth evaluation is on the market in TRAI’s session paper’s desk 2.1, titled ‘Composition of ARPU per 30 days—Wi-fi Service’. ARPU is a key metric for gauging the monetary viability of the telco.

From TRAI’s evaluation, it may be seen that the info income has gone up from Rs 10.02 per person to Rs 125.05 per person—a rise of about Rs 115 per person, a 12-fold development. Throughout the identical interval, income from calls decreased by about Rs 58 and income from SMS by about Rs 3.76. Nonetheless, the income improve from knowledge utilization has greater than compensated for the discount in name and SMS income and has supplied a residual surplus. Not related with OTTs, rental income has decreased from Rs 19.5 to Rs 8. Nonetheless, as already famous, all reductions have been worn out by the increase in knowledge revenues, leaving a wholesome general acquire—the online ARPU having risen from Rs 111.45 to Rs 141.14, which is a rise of 27%.

![]()

The evaluation of the TRAI knowledge clearly illustrates a discovering of the Worldwide Telecommunication Union (ITU)—“By creating worth for customers, world apex telecom physique, OTTs stimulate demand for broadband networks and companies… availability of OTTs create a virtuous cycle that will increase the worth of broadband community companies and thereby drives additional take-up and adoption of upper worth knowledge plans…OTT purposes drive the demand for web connectivity companies thus rising visitors and, consequently, the income of telecommunication service suppliers.” (ITU-D Report, 2021).

You will need to respect that cellular tariffs are left to open market forces and TRAI follows the forbearance strategy. Therefore, telecom operators are free to set the tariffs as per their want whether or not it’s for calls, knowledge, leases, value-added-services, or roaming. Whereas coping with tariffs, one is of course compelled to additionally look at prices. ITU findings on this respect are fascinating. Whereas web visitors development has been wholesome, related unit prices for key-traffic-dependent objects of apparatus have declined 12 months after 12 months and greater than offset any improve in gear required to hold community visitors. For the cellular community, the mixed impact of elevated traffic-dependent gear volumes and declining unit price seems to be consistent with the rise in month-to-month value paid by customers (ARPU). The conclusion by ITU is that “In neither case are there indications of market failure.”

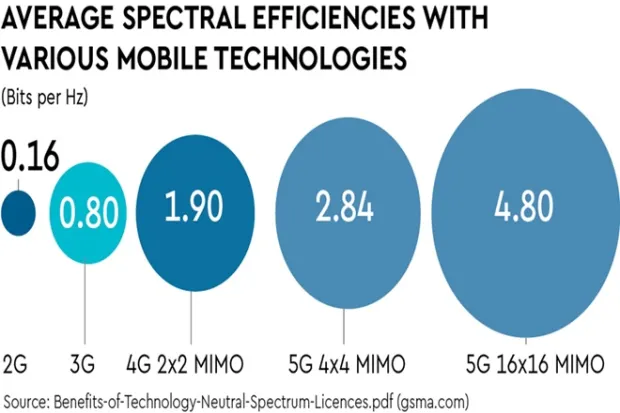

There’s the added huge bonus of vastly improved spectrum efficiencies over time. It’s a longtime undeniable fact that common spectrum efficiencies have risen plain vanilla GSM 0.16 Hz via 3G’s 0.80 bits per Hz, 4G’s 1.90 to 5G’s 16×16 MIMO—a stupendous 30-fold improve.

Clearly, we will count on a considerable trickle-down impact from the larger spectral efficiencies to the community price discount. Equally, there have been giant efficiencies within the spine networks, typically primarily based on optic fibre, because of which bandwidth prices have declined considerably. For instance, 10 GigE costs fell 18% and 100 GigE by 30%, compounded yearly from 2018 to 2021.

As ITU factors out, customers see OTT companies as providing higher value/efficiency, or as providing larger shopper welfare. It must be remembered that societal welfare is the sum of producer and shopper welfare. For OTT companies, the related advantages to producers are additionally excessive since their coffers are flowing plentifully from elevated general consumption of community companies in addition to an elevated variety of subscribers resulting from larger attractiveness of the companies.

European regulator BEREC’s findings in 2022 are much like ITU’s—community visitors is “triggered” by telco clients, driving the demand for broadband. They additional discovered no proof of “free using” and that the prices for web connectivity are sometimes coated and paid for by the telco clients. No regulatory intervention is critical. Through the years from 2015-2022, in India too, each TRAI and DoT have, with reasoning, kept away from intervention.

Clearly, community operators owe a lot to OTTs for his or her knowledge revenues upsurging and general ARPU rising. As cited by TRAI, ITU has additionally discovered that each sectors “engender advantages for one another in a symbiotic, complementary and mutually reinforcing method…and…each sectors have invested closely within the infrastructure to assist it.” In such a situation, one wonders concerning the wasteful arguments and pointless hostility.

The author is honorary fellow, IET (London), and president, Broadband India Discussion board

Views are private