The entry of broadcasters and huge OTT platforms into India’s micro-drama section is shifting the aggressive construction of a class that has scaled quickly on the again of mobile-first consumption, low-cost manufacturing and subscription-led monetisation.

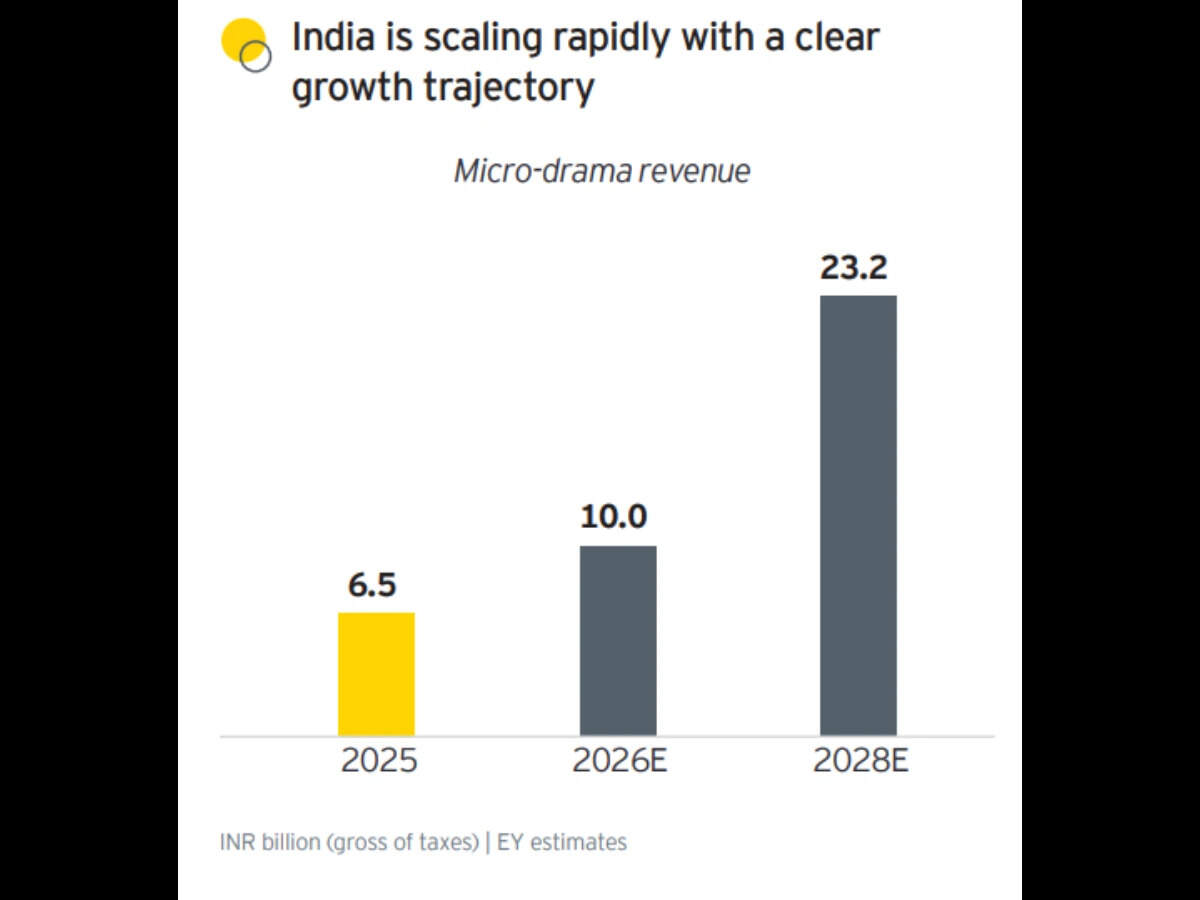

In keeping with the FICCI-EY media and leisure report, India’s micro-drama market was valued at INR 6.5 billion in 2025 and is predicted to develop at over 50 % yearly by 2028. The format has expanded rapidly, with India accounting for 11 % of worldwide downloads in Q1 2025, reaching 35 million downloads and recording a 113 % quarter-on-quarter enhance.

In China, the class has already scaled right into a multi-billion-dollar market, with revenues exceeding the nation’s field workplace, signalling the potential trajectory for India.

In India, progress has been pushed by Tier-II and Tier-III markets, which account for 60–75 % of customers, and by a younger viewers base, with 80 % of viewers between 18 and 34 years of age. Each day watch time ranges between 40 and 90 minutes, with completion charges exceeding 90 %, indicating sturdy engagement.

This early progress has largely been led by platforms comparable to Kuku TV and Story TV. Nonetheless, the launch of micro-drama choices by platforms comparable to the most recent entrant within the class– JioHotstar with Tadka, alongside initiatives from Zee Leisure with Bullet and Amazon MX Participant’s MX Fatafat, is predicted to change the economics of the class.

Distribution versus depth

The important thing shift lies in distribution. Giant platforms carry current person bases, cross-platform visibility and bundled pricing, giving them a structural benefit over impartial platforms apps.

Nitin Burman, group CRO, Balaji Telefilms, mentioned broadcasters and huge networks have the flexibility to soak up prices and combine micro-dramas into broader choices. “They’ll supply micro-dramas as half of a bigger content material bundle, usually at no further value,” he mentioned. Balaji Telefilms launched Kutingg final 12 months, an OTT platform that includes short-form video content material alongside different codecs.

This creates a pricing strain level for impartial platforms that depend on direct subscriptions and microtransactions. Business executives mentioned the central query is whether or not customers will proceed to pay individually for micro-drama apps if comparable content material is offered inside bigger ecosystems.

Ambuj Kashyap, EVP, microcontent at JioStar, mentioned the corporate’s strategy is to combine micro-content throughout the broader JioHotstar platform. “Being a part of the ecosystem permits us to satisfy our customers the place they’re, throughout codecs and moments,” he mentioned, including that “attain can speed up adoption, however it can not maintain engagement.”

The shift from impartial platforms to bundled consumption is according to earlier phases of the OTT market, the place aggregation and bundling reshaped person behaviour.

Early mover benefit

Early scale was pushed by impartial platforms by high-volume content material, data-led personalisation and targeted product design.

Saurabh Pandey, founder and CEO, Story TV, mentioned the platform has scaled quickly on content material quantity and engagement. “We’ve got crossed 1,200 authentic dramas and are producing 150–200 reveals a month,” he mentioned. The platform has recorded over 80 million installs in six months, with common person time spent of round 90 minutes per day.

Pandey mentioned early entrants have a bonus in understanding person behaviour and constructing knowledge capabilities. “Micro-drama depends closely on knowledge, understanding when to position a cliffhanger or twist,” he mentioned.

Sachin Singh, head of Kuku TV, mentioned the format requires steady iteration and excessive content material velocity. “Success depends upon understanding client insights, genres and storytelling codecs. This takes time to construct,” he mentioned.

Kuku TV presently has over 10 million paid subscribers and has crossed 180 million downloads. The platform releases over 300 micro-drama titles every month and is concentrating on increased output.

Nonetheless, as broadcasters enter, this benefit could slim. Chandrashekar Mantha, accomplice and media and leisure sector chief, Deloitte India, mentioned the competitors will evolve right into a steadiness between agility and scale. “Early platforms benefited from product–market match, however bigger gamers carry stronger distribution and built-in ecosystems,” he mentioned.

Kashyap added, “What actually drives this class ahead is content material that’s designed for the format, with sturdy storytelling, consistency, and relevance to how audiences are consuming right now.”

Content material scale and value economics

The class has scaled on low manufacturing prices and excessive output. Business estimates counsel micro-drama manufacturing prices vary between INR 12 lakh and INR 18 lakh per collection, relying on scale and casting. As compared, typical OTT reveals sometimes value upwards of INR 50 lakh to INR 1 crore per collection. Marquee titles and premium originals run considerably increased relying on expertise, manufacturing design and episode depend.

Business estimates counsel round 500 micro-drama episodes are produced month-to-month in India, translating to just about 800 hours of authentic content material in 2025.

This has enabled platforms to experiment quickly throughout genres comparable to romance, crime, fantasy and mythology. Tier-II audiences have proven a desire for aspirational themes, together with prosperous life and fast success narratives, whereas Tier-I audiences are starting to demand extra various storytelling.

Singh mentioned the following part would require innovation past early tropes. “Standard codecs comparable to romance and revenge are saturating. Future progress will depend upon figuring out new genres,” he mentioned.

Pandey added that the class is already increasing into political and company narratives, indicating a shift from early mass codecs to extra numerous storytelling.

Nonetheless, rising competitors could result in value pressures. Deloitte’s Mantha mentioned supply-side growth may end in content material fatigue and better manufacturing prices, particularly as platforms compete for expertise and scale.

Monetisation fashions in flux

Monetisation stays fragmented. In India, the market has been led by subscriptions, cash and microtransactions, supported by UPI AutoPay.

The FICCI-EY report famous that 70–80 % of subscribers authorise recurring funds by UPI mandates, and as much as 60 % are prone to drop with out it. Promoting presently contributes lower than 15 % of income however is predicted to develop.

In keeping with Kashyap, monetisation buildings work finest once they comply with real engagement, not the opposite means round.”

Singh mentioned Kuku TV has expanded past subscriptions into pay-per-view and ad-supported fashions. “There may be sturdy demand, however not all customers are prepared to pay but,” he mentioned.

Kashyap mentioned promoting is prone to scale first for bigger platforms. “The response from manufacturers has been sturdy, notably for built-in content material codecs,” he mentioned.

Neha Markanda, chief enterprise officer, ShareChat and Moj, mentioned micro-dramas are rising as a format for model integrations, with increased view-through charges and recall in comparison with conventional codecs. She added that ad-led ecosystems may develop into dominant because the class scales. ShareChat operates the micro-drama app QuickTV and is an early entrant.

She added that “as established OTT gamers enter, the class will develop additional into a mixture of AVOD and SVOD fashions. Nonetheless, we consider there’s ample room for a number of platforms, particularly these constructed for culturally rooted, language-first audiences. Our focus is on constructing a deeply related content material and monetisation ecosystem, powered by creator-led storytelling and scaled distribution.”

World developments point out a mixture of monetisation approaches. Deloitte expects India to undertake a blended mannequin combining ad-supported viewing, microtransactions and selective subscription bundling, slightly than converging on a single format.

Shopper behaviour and format shift

Micro-dramas are positioned between social video and long-form OTT. Consumption is fragmented throughout a number of quick periods slightly than lengthy viewing home windows.

Pandey mentioned customers sometimes open the app a number of occasions a day, with periods lasting 20–half-hour. Singh mentioned the viewers overlaps with OTT however is pushed by mobile-first behaviour.

The format has additionally been positioned as a structured various to short-form video. Burman mentioned platforms have addressed the invention problem seen in earlier codecs comparable to Reels and Shorts by creating steady, episodic storytelling.

Nonetheless, recall stays low. Burman famous that viewers usually don’t bear in mind present names and that peer dialogue is proscribed in comparison with long-form content material.

This impacts the flexibility to construct franchises and long-term mental property, which stays a key benefit for conventional OTT and broadcast codecs.

Consolidation probably

Business executives anticipate consolidation over the following one to 2 years.

Burman mentioned the market may slim to 4 to 5 main gamers, much like the OTT section. Pandey mentioned two to 3 platforms are prone to dominate over time.

The entry of broadcasters could speed up this course of by rising competitors on each pricing and content material scale.

On the similar time, regional growth stays a key progress lever. Burman mentioned platforms that develop into a number of Indian languages can considerably enhance their person base.

The FICCI-EY report additionally highlighted that fifty % of customers want content material in native languages, reinforcing the significance of localisation.

Strain shifts to pricing and retention

For the platforms comparable to Kuku TV and Story TV, the following part will depend upon retaining differentiation in a market the place distribution is now not a constraint.

Their strengths lie in content material velocity, data-led personalisation and product design tailor-made to short-form consumption. Nonetheless, they face strain on pricing and person acquisition as bigger platforms bundle micro-drama inside broader choices.

Singh mentioned capital alone doesn’t decide success on this format. “Past some extent, success depends upon storytelling and engagement,” he mentioned.

Pandey mentioned the winner would be the platform with the very best engagement and retention. “The platform that captures the most important share of time and pockets will lead,” he mentioned.

In keeping with Kashyap, over the following 12 months, what is going to outline success in micro-content is the shift from novelty to behavior. He added that sustained engagement will depend upon constant, high-quality storytelling at scale.

Whereas Mantha mentioned long-term success will depend upon value effectivity, differentiated storytelling and the flexibility to construct repeatable monetisation fashions.

As broadcasters and OTT platforms scale their presence, micro-drama is transferring from an impartial platforms class to a part of a wider content material ecosystem. The end result will decide whether or not impartial apps stay viable or develop into a part of bigger platforms by consolidation or partnerships.