Erik Khalitov/iStock Unreleased through Getty Photographs")

The next explores the potential 30% headcount discount at Warner Bros. Discovery’s (NASDAQ:WBD) advert gross sales division. We carry out valuation and basic affect analyses on materials information headlines inside a 12-hour turnaround framework in our Market service, much like the dialogue under.

Introduction

Following the abrupt shutdown of the merely weeks previous CNN+ information streaming platform underneath Warner Bros. Discovery’s new post-merger management, the mixed entity’s advert gross sales division was referred to as up subsequent to the chopping block. The corporate was reported earlier this week that will probably be lowering the division’s headcount by 30% within the close to time period, coinciding with mounting information of hiring freezes and layoffs throughout all industries forward of upcoming macroeconomic uncertainties.

WBD inventory has but to point out a turnaround that many have been anticipating submit merger, given its burgeoning streaming enterprise, management in media and leisure, industry-leading advert attain, and extremely coveted content material library. In reality, the inventory is headed towards among the lows final seen since previous to the WarnerMedia-Discovery merger announcement on a per share foundation. WBD has misplaced virtually half of its market worth since finishing the spinoff as a consequence of unprecedented macro challenges spanning document inflation, quantitative tightening, ongoing COVID outbreaks, and an intensifying warfare in Ukraine.

Though the most recent information of advert gross sales job cuts at WBD could also be sparking renewed issues of softening advert spending this yr as a consequence of dampening client sentiment forward of a potential recession, the magnitude and execution timeline of the endeavor alerts that it could actually simply be a part of the corporate’s post-merger expertise consolidation plans. The current growth on job cuts in WBD’s advert gross sales division, which contributes to the vast majority of its annual revenues, will not be anticipated to drive a cloth change to the corporate’s valuation prospects. As an alternative, the continued realization of $3+ billion in anticipated post-merger value synergies will bolster WBD’s long-term upside potential by enhancing its basic strengths, although present macro headwinds will possible proceed to weigh on the broader know-how and digital media sector’s efficiency within the close to time period.

What’s Warner Bros. Discovery Doing to Its Advert Gross sales Staff?

Reviews have been circulating that WBD will probably be executing a plan to scale back its advert gross sales headcount by as much as 30%. The plan includes extending “buyout presents” to U.S. advert gross sales workforce personnel starting this week, encouraging voluntary exits versus direct layoffs. The execution timeline has but to be disclosed, nevertheless it has been reported that WBD plans to scale back its present international advert gross sales headcount of three,000 to round 2,000 “over time.”

The most recent growth coincides with a sequence of hiring freezes and layoffs noticed throughout the {industry} with a purpose to minimize prices and put together for a possible development slowdown amid sprawling macro challenges. Paired with indicators of softening in advert spending this yr as a consequence of waning client sentiment amidst rising inflation and aggressive financial coverage tightening that dangers an financial recession, WBD’s newest spherical of advert gross sales job cuts are elevating issues about whether or not its core income driver could also be slowing.

What are the Headwinds on Advert Spending?

Based mostly on the newest monetary efficiency at WarnerMedia and Discovery previous to their merger, promoting accounted for 18% and 47% of complete revenues, respectively. Promoting has been a core power for WBD, given its diversified advert distribution channels, which all boast industry-leading attain. But, WBD’s heavy reliance on advert revenues have additionally concurrently drawn questions on its publicity to near-term dangers of a slowdown in advert spending alongside waning client sentiment.

Forecasts for complete international promoting spending this yr have been on a rolling decline in response to the financial system’s struggles with maintaining inflation in examine given extraordinary circumstances that embrace a protracted pandemic and Russia’s invasion of Ukraine. Main media intelligence MAGNA International has trimmed its prediction on international advert spending development this yr from 12% to 9% amid rising dangers of a structural financial downturn later this yr. This compares to international advert spending development of +23% year-on-year in 2021 (U.S. +26% y/y), buoyed by a short stint of post-pandemic financial restoration.

Nevertheless, WBD’s management in international advert distribution is predicted to scale back among the near-term affect in weakened advert spending. The anticipated development deceleration in advert spending via digital media codecs like video / over-the-top (“OTT”) streaming and conventional media codecs like payTV and cinema, which WBD leads in, will probably be comparatively much less pronounced in comparison with different distribution channels like social media platforms.

In linear TV, WBD presently attracts probably the most prime-time viewership than all of ABC, CBS, NBC and Fox mixed. This positions the corporate favorably for the 22% of complete annual advert spend allotted to TV commercials. The rising subscription base of HBO Max and discovery+ additionally makes them engaging sources for the rising shift in advert spending in direction of digital platforms.

Video streaming platforms are actually house to about 23% of complete advert spend within the U.S., and the determine is predicted to broaden additional as digital promoting’s greater than 60% share of the broader promoting market as we speak is projected to develop at an 11% CAGR via 2030. The intense outlook on video streaming advert spend is additional corroborated by MAGNA’s predictions – advert spending via video streaming / OTT platforms will expertise the quickest development in comparison with different distribution channels in 2023 (estimated at +30% y/y), which underscores robust tailwinds for WBD’s core promoting enterprise over the longer-term.

Why is WBD Chopping Its Advert Gross sales Headcount?

Though current information of WBD’s determination to chop its advert gross sales headcount coincides with a sequence of hiring freezes and layoffs noticed throughout the {industry} to organize for unsure financial situations forward, the prolonged timeline of WBD’s newest endeavor could indicate in any other case. Regardless of the anticipation for softening advert spending this yr, which may affect the core income driver at WBD, the most recent job cuts in advert gross sales is probably going a results of beforehand deliberate post-merger expertise consolidation efforts. The corporate has deliberate to attain a minimum of $3 billion in value synergies following the WarnerMedia-Discovery merger by the top of 2023.

Wanting on the prolonged timeline of the speculated job reductions, which will probably be executed via phases (i.e. buyout supply, layoff, and pure attrition), it traces up with WBD’s greater image plans for realizing post-merger value synergies versus swift layoffs to right away decrease near-term working prices. The most recent growth additionally aligns with WBD CEO David Zaslav’s earlier feedback that “the corporate’s advert gross sales phase presents a chance for cuts as a consequence of loads of overlap in roles post-merger,” in addition to CFO Gunnar Wiedenfels’ plans to scale back duplication within the $5+ billion of annual advertising and marketing spend by the mixed firm. The choice to consolidate and scale back extra advert gross sales headcount is additional corroborated by the approaching mixture of HBO Max and discovery+, alongside different operational and geographical segments, to materialize efficiencies going ahead.

The most recent advert gross sales headcount discount, much like the shutdown of CNN+ in April, is probably going only the start of extra aggressive, however calculated, measures to maximise realization of post-merger value synergies. That is particularly important given the corporate’s formidable deleveraging targets – WBD is presently concentrating on gross leverage of two.5x to 3x inside 24 months of finishing the merger.

For instance, the choice to drag the plug on CNN+ after investments of $300+ million by earlier administration was undoubtedly not a simple feat for each the corporate’s leaders and traders to digest. But, it did forestall further spending of $700 million from the initially authorized $1 billion price range for a venture that possible is not going to generate significant returns inside an inexpensive timeline. It was additionally a prescient transfer that has lowered WBD’s publicity to a possible subscription slowdown forward of tightening client budgets as a consequence of rising inflation.

The following spherical of inevitable job cuts that is going to make headlines will possible be associated to WBD’s streaming enterprise, as administration strikes ahead with the approaching merge of HBO Max and discovery+. The anticipated value financial savings realized there can even complement the gross sales synergies from the merge of two of the biggest streaming content material libraries, which is a double-plus for WBD’s long-term basic and valuation prospects.

The choice to merge HBO Max and discovery+ additionally comes as a well-timed determination, as competitors heightens in direct-to-consumer (“D2C”) streaming providers, whereas customers’ wallets slim down as a consequence of rising dwelling prices. Along with streaming pure-plays like Netflix (NFLX), Hulu (DIS) and Apple TV+ (AAPL), many conventional leisure and media firms much like WBD have additionally launched their very own platforms, akin to Paramount+ (PARA) and Peacock (CMCSA). However the variety of providers that households are prepared to pay for is restricted, particularly as client sentiment dampens forward of rising inflation and a possible financial recession:

In streaming, now we have a large alternative to achieve the widest potential addressable market by providing a spread of tiers, all with probably the most compelling and full portfolio of content material. A premium and attractively priced ad-free direct-to-consumer product, a lower-priced ad-light tier, one thing now we have had great success with and is our highest ARPU (“common income per person”) product, and a few very price-sensitive markets outdoors america, we will even supply an advertiser-only product.

Supply: WBD 1Q22 Earnings Name.

Continued execution of WBD’s aggressive value and gross sales synergy realization technique, particularly underneath the experience of media and leisure veterans which have proven a optimistic observe document in turning Discovery right into a “free money circulation machine,” exhibits promising potential for redirecting the corporate again on observe in direction of optimistic shareholder worth.

How A lot will WBD Save from Advert Gross sales Job Cuts?

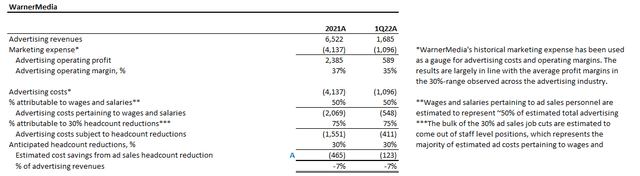

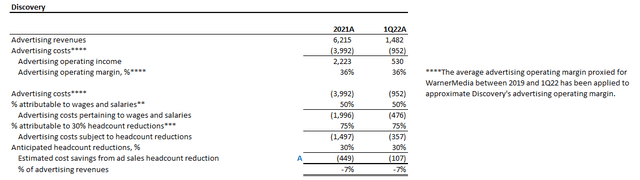

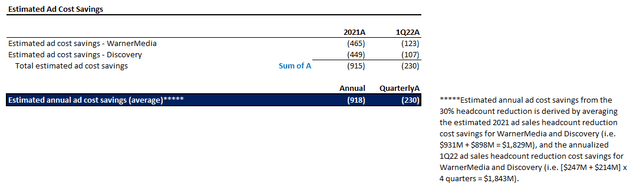

Whereas every of WarnerMedia and Discovery had disclosed their respective promoting revenues previous to the merger, an in depth breakout of prices pertaining to the phase’s gross sales has not traditionally been offered. Based mostly on a excessive stage, back-of-the-napkin calculation, we anticipate the upcoming 30% discount to advert gross sales headcount to yield near $1 billion in annual value financial savings, representing a few third of administration’s focused $3 billion in annualized post-merger value synergies.

The estimate is derived as follows:

Estimated promoting value financial savings (Creator)

- Now we have taken advertising and marketing bills pertaining to historic WarnerMedia operations as a proxy for promoting income associated prices. The ensuing promoting working margin of 35% to 37% noticed in 2021 in 1Q22 is in step with the common revenue margins within the 30%-range (vs. best-in-class margin of ~50% at $TRMR) noticed throughout the promoting {industry}.

- Leaning on the moderately conservative aspect, we estimate half of promoting prices are straight attributed to advert gross sales personnel wages and wage expense. This represents ~$2.1 billion in 2021 and $550 million in 1Q22 at WarnerMedia.

- A lot of the 30% advert gross sales job cuts are anticipated to come back out of the operational workers stage. As such, we estimate 75% of estimated advert gross sales personnel wages and wage bills to get a 30% discount in accordance with the deliberate job cuts.

- In consequence, the upcoming job cuts in WBD’s advert gross sales division pertaining to legacy WarnerMedia advert gross sales workers will add again about 7 proportion factors to promoting margins.

Estimated promoting value financial savings (Creator)

- Now we have taken the common historic promoting working margin of ~36% estimated for WarnerMedia above as a proxy for promoting income associated prices at Discovery.

- The assumed % of estimated promoting prices associated advert gross sales personnel wages and wage bills, and the assumed % of attributable to the upcoming job cuts is in step with the respective 50% and 75% utilized within the WarnerMedia calculation above.

- In consequence, the upcoming job cuts in WBD’s advert gross sales division pertaining to legacy Discovery advert gross sales workers will add again about 7 proportion factors to promoting margins.

Estimated promoting value financial savings (Creator)

- Averaging the estimated annual and quarterly advert value financial savings from upcoming job cuts based mostly on WarnerMedia and Discovery’s precise 2021 and 1Q22 monetary efficiency, we predict near $1 billion in annualized value synergies from merging the 2 legacy advert gross sales groups. This represents near a 3rd of WBD’s focused $3 billion in annualized post-merger value synergies.

WBD Inventory Valuation Implications

As mentioned within the foregoing evaluation, we imagine WBD’s upcoming 30% headcount discount in its advert gross sales division will not be an indication of downsized development, however quite an elimination of extra spending, which is a plus for its valuation prospects. On this foundation, we’re sustaining our post-spinoff worth goal of $45 for the inventory, which is derived based mostly on consideration of administration’s focused $3 billion in annualized value synergies, $52 billion in consolidated revenues, and $14 billion in consolidated EBITDA by 2023. The PT represents upside potential of greater than 220% based mostly on its final traded worth of $13.98 on June 14.

Even underneath the present market local weather the place valuation multiples have contracted throughout the board in response to tightening financial situations, WBD continues to commerce at its pre-merger, steep low cost to the digital media and leisure, and video streaming providers peer group. The low cost will not be reflective of WBD’s capacity to generate optimistic working and free money flows, in addition to its basic development prospects buoyed by its main market share in advert gross sales, content material distribution, and D2C video streaming. Though present macro headwinds will possible proceed to weigh on the broader know-how and digital media sector’s efficiency within the close to time period, which can consequently affect WBD’s near-term inventory efficiency, we stay optimistic on its long-term valuation prospects.

Conclusion

In distinction to the slew of hiring freezes and job cuts throughout the non-public sector in response to a looming financial recession, WBD’s discount of its advert gross sales headcount is probably going a part of its beforehand deliberate efforts in maximizing post-merger value synergies. The eradicated overlap in advert gross sales expertise is not going to solely enhance the consolidated firm’s backside line going ahead, nevertheless it additionally will streamline operations to make sure sufficient capitalization of a back-end loaded yr in promoting.

Whereas advert spending has weakened within the first half of the yr as a consequence of dire macroeconomic situations, seasonality-driven development from back-to-school and vacation adverts, alongside the addition of political advert spending later this yr within the U.S. will possible assist recoup among the {industry}’s losses, which makes a good surroundings for industry-leading advert distributor WBD. Political advert spend forward of midterm elections later this yr is predicted to achieve $6.7 billion, a document 52% enhance from 2018. Greater than $4 billion of the estimated political advert spending later this yr is forecast to be spent on distribution via payTV and video streaming / OTT platforms, enjoying proper to WBD’s strengths.

Paired with the corporate’s continued self-discipline in bolstering its steadiness sheet and basic development trajectory, the inventory stays on optimistic observe in direction of realization of promising upsides over the long run.